Idea Brunch with Geoffrey Seiler of MLPs and More

Welcome to Sunday’s Idea Brunch, your weekly interview series with underfollowed investors and emerging managers. We are very excited to interview Geoffrey Seiler!

Geoffrey is currently the author of MLPs and More, a newsletter focused on the MLP sector, and Bull vs Bear, which is focused mostly on long ideas, but a few short ideas as well. Before launching his newsletters, Geoffrey worked as a senior analyst at Raging Capital Management and before that served as the editor of the Bull Market Report.

Geoffrey, thanks for doing Sunday’s Idea Brunch! Can you please tell readers a little more about your background?

Thanks for having me, Edwin. I probably took one of the most circuitous routes to becoming an equity analyst at a hedge fund ever, graduating with a History degree. After working some entry-level jobs at places like Vanguard and Bloomberg, I eventually stumbled across a job posting for a financial copy editor position for a company run by investor Bill Martin, who taught me an enormous amount about investing. While working for Bill, I went from being a copy editor to running The Bull Market Report when he started his hedge fund Raging Capital.

The Bull Market Report was a daily investment newsletter that had a mock portfolio of about 50 long ideas. When Bill started his fund, I became responsible for all the stock picking and daily content, as he was no longer able to be involved in that part of the business. I took over a few months before the Great Recession, so it was really a baptism by fire. Running a daily newsletter, I learned to process a lot of information quickly to get to what was most important for a particular company and industry.

Many of the subscribers to The Bull Market Report were very interested in dividend stocks, which is why the midstream sector and MLPs became a particular focus for me, given their traditionally high yields. I later took this knowledge to pitch Crestwood Equity Partners (NYSE: CEQP) at the fund, which became one of Raging Capital’s top-contributing positions while I was at the firm.

While at Raging Capital I really honed my skills working with some top-investment minds. It was a long-short fund that generated a lot of alpha on the short side, and I learned an incredible amount.

That is quite an unusual path. Do you think the path you took impacts the way you look at investments?

Yes, I’m not a classically trained business school graduate, I went to a liberal arts college and graduated with a degree in History. I think that allows me to view things a bit differently.

One strategy I’ve employed that has been successful on the long side is investing in unloved companies that are going through business transformations. Past history often clouds investors’ judgments, so they can miss shifts in individual companies, as well as industries. Often these stocks are undervalued because of the way they did things in the past.

These stocks get sent to the penalty box, and it can take years for them to get out. But when they do, you get a growing business with a stock that is re-rating, which is a great combination that leads to a lot of upside.

Sometimes investors can overcomplicate things and miss the forest through the trees. At the end of the day, you need to simply answer if it makes sense. Does management’s strategy make sense? Does the valuation make sense?

And then you also can’t pretend that companies operate in a vacuum. The macro-environment is important and can’t be ignored.

Why did you decide to launch a newsletter focused on MLPs?

As for MLPs and midstream stocks, I feel this is a specialized area that is generally underserved. And just to be clear, MLPs are the structure many midstream energy stocks adopted. Some have since converted to C-corps, but they are still generally referred to as MLPs, even though they technically aren’t partnerships anymore.

The sector got a bad rap several years ago that was largely deserved. In the past, general partners (GP) would take advantage of LP holders in a few ways. This came mostly through GPs owning incentive distribution rights (IDRS) where LPs would have to pay the GP when distributions reached a certain level. Once IDRs got to the typical 50/50 high split, the LP was paying double for any incremental distribution increase.

This pushed many GPs to have their LPs aggressively grow their businesses and distributions. About 10-15 years ago, it wasn’t uncommon to see MLPs diluting holders via 2-3 equity raises a year. At the same time, distribution coverage ratios were kept slim and leverage high. When the energy industry began to struggle, this led to a lot of issues for a number of midstream companies.

However, that difficult energy environment changed both the midstream space, as well as how E&Ps operated. MLPs eliminated IDRs, cut distributions to focus on their balance sheets, and slowed growth. It’s now a much healthier industry today without the conflicts of interest of the past, yet the stocks generally do not reflect this in their valuations.

The energy industry has also changed. U.S. energy producers learned valuable lessons in the past decade and don’t look ready to chase theoretical IRRs at the expense of cash flow even with high oil and natural gas prices. Slow and steady now wins the race. Meanwhile, the oil supply is being impacted by years of underinvestment in new drilling exploration and activities, and renewable resources are still only making a pretty small dent in overall energy consumption.

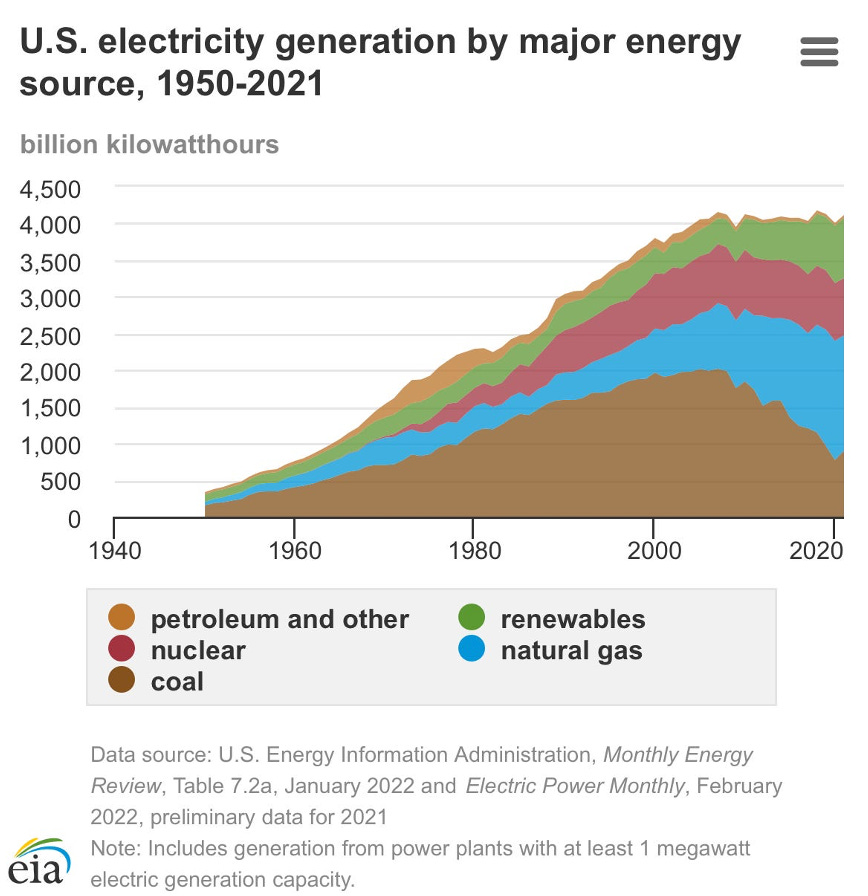

The energy group remains hated by investors and green advocates alike, but the transition to renewable fuels still looks to be a ways off. In fact, while the push to electrical vehicles (EVs) has been touted as green, the reality is that it’s mainly just been a shift from crude to natural gas at this point. The graph below shows how much share natural gas has gained in U.S. electric generation, and of course, electricity is what powers electric vehicles.

Thus, I really think energy stocks, including midstream, are very well set up to outperform for quite some time. At the same time, it remains one of the most underweight sectors out there.

What are the key ingredients for success when investing in MLPs? Are there any common red flags to avoid?

The biggest key is getting to know a company’s assets. Are they in the right basin, what customers are using them, are there any competing solutions, how are the contracts structured and how long do they run? Then you want to look at things like leverage, cash flow generation after distributions, and growth opportunities.

My work on Crestwood (CEQP) while I was at Raging Capital was a good example of this. It was a broken stock at the time, and while some of its assets were lower quality, it also had some very high-quality ones as well. Most people weren’t willing to do the work and dive into the company and look at it on an asset-by-asset basis, which gave us a real advantage. It eventually sold a scarce asset we had identified for an attractive price, which started a turnaround for the company, and a huge rally in the stock. Today, the company has completely transformed itself.

On the other side of the coin, companies with ties to a struggling basin can be a red flag. This is especially true if it has contracts, or minimum volume commitments (MVCs), that are set to expire. Given the current interest rate environment, I’d also be mindful of any companies that have a lot of debt expiring soon, or floating rate debt about to reset.