Idea Brunch with Andrew Walker of Rangeley Capital

Andrew Walker shares his research process, opinion on SPACs, and his best idea

The paywall has been removed from this Idea Brunch interview. If you want an interview like this in your inbox every Sunday at 1pm ET, please join Sunday’s Idea Brunch for $70/year.

Welcome to Sunday’s Idea Brunch, a weekly interview series with underfollowed investors and emerging managers. We are very excited to interview Andrew Walker!

Andrew is currently the head of research and a portfolio manager at Rangeley Capital, a special situations and value fund based in New Canaan, CT. In addition to running Rangeley Capital, Andrew also hosts the popular Yet Another Value Podcast, writes the Yet Another Value Blog, and was the winner of the 2018 Ira Sohn Idea Contest. Prior to joining Rangeley Capital in 2015, Andrew was an associate at Sankaty Advisors and a senior analyst at McKinsey.

Andrew, congrats on your huge success building a following online. In addition to 20,000+ followers on followers on Twitter, you also have a popular podcast and newsletter. Why did you decide to start sharing educational material online? And do you think your podcast, Twitter, and newsletter have helped you become a better investor?

Well, thank you for having me! I’m a big fan of Sunday’s Idea Brunch.

I started writing online for a bunch of reasons. I think the top one would be I love it; writing is how I think and process things, and writing online has helped me make friends and acquaintances I never would have met without it. I’m a big believer in the online world; my top advice for almost every investor I know trying to break into the industry is to put their stuff online.

Yes, I think the podcast / Twitter / newsletter have definitely helped me become a better investor. Twitter has helped with networking and microphone amplification; I don’t have the largest following (somehow, I’m less than half of yours!), but I have a large enough following that I can get eyeballs on a situation if needed. The podcast has helped me quickly get up to speed on a bunch of different interesting ideas, as well as meet some new investors. And the newsletter helps me refine my thinking and often serves as a great way to get feedback on ideas; I can’t tell you the number of times I’ve written about a company saying “this is interesting, but I don’t quite get this one part” and gotten contacted by a large shareholder eager to swap thoughts.

You’ve now interviewed over eighty investors on your podcast and discussed their stock pitches. What are the key ingredients for a successful investment and investor?

The interesting thing about the podcast is how different all of the investors are. Some of them are running growth strategies, some run deep value, some run event books. It’s cliché, but I think the obvious key is that the investors who do the best have put lots of research into the companies they invest in, and that research gives them the conviction to swing hard at their best ideas when they think something is mispriced. I think that shows in the podcast; you can tell the difference between a guest who has really thought about a company and someone who is just YOLO’ing a position. The best guests have answers to almost every question I ask because they’ve thought deeply about a company; the worst guests respond “I don’t know” or spitball on questions constantly because they haven’t really thought about a company. There’s nothing wrong with saying “I don’t know”, but if you have a huge position and your answer to three major risks is “I don’t know” or “I haven’t thought about that,” then…… well, not good!

You’ve also written a lot about SPACs. What advice would you give to an investor that wants to dig into the SPAC market and differentiate the good ones from the bad ones?

I’m endlessly fascinated by SPACs. The thing that really attracts me to them is the optionality: you buy a SPAC for ~$10/share, and then you wait for them to announce a deal. Some deals can cause the market to go bonkers (like the recent DWAC / Trump Media deal). If that happens, awesome! Sell your shares and make a big profit. If the market yawns at the deal, just redeem your shares for $10 and break even. Heads, you win, tails, you don’t lose (though there is some opportunity cost!).

That said, SPACs can be dangerous. I’ve talked about this before, but the incentives around SPACs are just awful. A sponsor will put up ~$5m of capital for a $200m SPAC. If the SPAC successfully completes a deal, the sponsor will make multiples of their money almost regardless of what the SPAC share price does. If the SPAC doesn’t complete a deal, the sponsor losses all of their money. So, sponsors are incentivized to do anything they can to get a deal over the finish line.

History suggests that buying SPACs and holding them through their deals (post de-SPACing) is a poor strategy. The average SPAC significantly underperforms the market and destroys value. So you want to be very careful holding SPACs through their deal; in fact, the base rate might be to just never hold a SPAC through a deal.

Still, there are always diamonds in the rough, and if you can identify “a diamond” the stock will often do really well very quickly. In general, to find one of those diamonds, you want to look for sponsors that are really aligned with shareholders (generally meaning they are writing big checks into their deals, whether from doing a big PIPE at the time of merger announcement or having a forward purchase agreement with the SPAC to buy shares at the same price as minority shareholders at deal time) and who have proprietary deal networks so that they are finding unique deals (most SPACs find their deals through banker processes, which is ripe for overpaying as the seller will generally just select the SPAC who will pay the most since all SPACs are basically the same).

What are two or three interesting ideas on your radar now?

I’ve talked extensively about cable companies on the blog (most recently here), so I won’t bore your readers by rehashing the thesis there. I will say that, across the globe, there is a massive discrepancy between the multiples public investors will put on cable assets and the multiples strategic or financial buyers are willing to pay in a take-private. That discrepancy cannot last forever; eventually, the cable companies will need to rerate higher or all of them will be taken private. Obviously not investing advice, but I think you could buy just about any cable company globally at the current multiples and do well on a multi-year horizon (there are a few exceptions).

For something different, I’m a long-time owner (bagholder?) of Ambac Financial Group (NYSE: AMBC — $709 million). The thesis for Ambac is pretty simple: at ~$15/share, the stock trades below book value (~$20/share), and book value is substantially understated as Ambac has outstanding litigation against BoA for securitized mortgages Countrywide (which BoA bought) underwrote that Ambac insured and lost a bundle on during the financial crisis.

Waiting for the lawsuit to play out has been like waiting for Godot; you can find old VIC write-ups from 2013 that thought a settlement with BoA was imminent. However, I believe we’re finally in the end game; the court recently set September 7, 2022 as the starting date for the trial. Traditionally, these suits have been settled right before the trial starts; in fact, I’m not aware of a single one of these lawsuits that did not settle.

A quirk of GAAP accounting means potential settlements tend to lead to massive gains. A lawsuit against a company often comes with statutory interest (i.e. if I sue you for $1B in damages, and the suit settles three years after the damages occurred, you’ll need to pay me the settlement costs plus three years of statutory interest). GAAP does not generally allow companies to book statutory interest on their balance sheet. The AMBC / BoA lawsuit stems from financial crisis-era mortgages, so if and when a settlement happens the gains from statutory interest alone should be huge.

Anyway, in the next year, I expect Ambac and BoA to settle their suit. Given how seasoned the Ambac / BoA case is, my base case is that a settlement will result in ~$1B in gains over where the suit is held on AMBC’s books. Including warrants, Ambac has just over 50m shares outstanding, so a settlement could result in ~$20/share in increased to book value (versus today’s share price of ~$15/share). In addition, with Puerto Rico having restructured and the BoA case settled, Ambac will be largely derisked, and I wouldn’t be surprised to see them sell the rest of their legacy business to Assured Guaranty on the heels of the settlement (similar to what peer Syncora did a few years ago).

Is there downside here? Yes, absolutely. If for some reason Ambac lost the trial, then it would not be pretty for the stock. However, the holding company has ~$6/share of investment assets plus some smaller subsidiaries they recently acquired, so the stock wouldn’t be a zero even in a disaster scenario. However, I find it extremely unlikely that AMBC would lose; again, we’ve seen tons of lawsuits from insurers against banks who underwrote financial crisis mortgages, and I’m not aware of a single suit that lost.

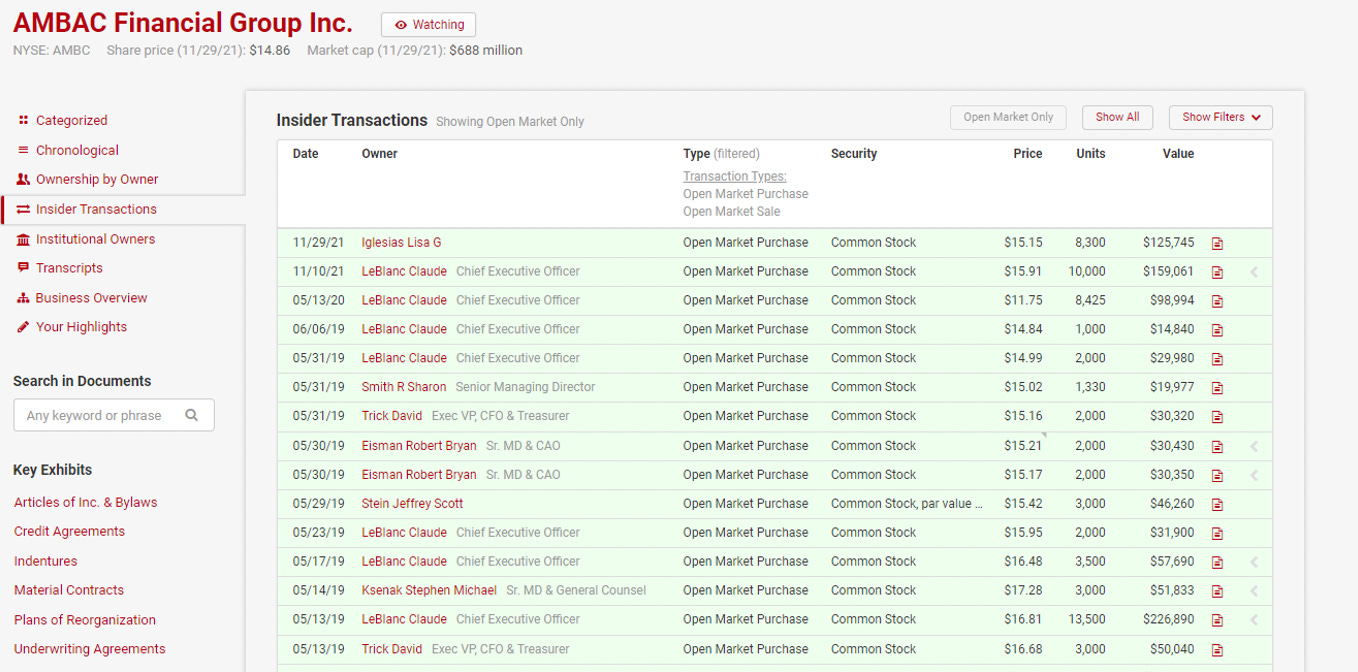

I’ll add a bonus note: insiders appear to agree here. I can’t find any examples of insider sales in the recent past, though I can find lots of (small) insider purchases, including two recent ones from a director and the CEO.

Andrew, what are some of the first things you do when researching a company? What does that first hour of research look like for you? Do you do anything that few others do?

Honestly, I don’t think I do anything few others do; I’d be interested if there’s some unique technique that only the real investing “ninjas” know about / practice. One thing I have been using increasingly over the past year is expert networks as the new “streaming” models like Tegus have made the cost much more reasonable for investors who aren’t writing >$100m checks for every investment (which was necessary to justify the cost of the old private call model). I have spent a lot of time thinking about how I use expert networks and how to use them better; if anyone has any advice or wants to swap notes, I’d certainly love to hear them.

Anyway, back to looking at a new company. I’d say the vast majority of ideas come from two places: a friend pings me about a company with an investment thesis, or I’m researching one company and as a natural progression to that research I start moving into another company (I.e. I’m looking at a cable company, so as a natural extension I’ll look at a peer cable company to see what’s different about them or research a competitor like a telecom company). So, I’m generally looking at a “new” company with at least some background knowledge of the company or the sector.

I’ve switched the way I approach new companies over time. I used to start by reading the 10-K; now I’ll generally start by reading the most recent investor day and/or transcript from a conference they recently attended, then their most recent earnings report and earnings call, and then transition to the 10-k.

What would you like Rangeley Capital and your content businesses to look like 10 years from now?

Is “larger” too trite?

In all seriousness, looking back ten years from now I’d like Rangeley to outperform the indices, hopefully substantially. I guess that’s pretty trite too, but isn’t that the goal of any manager?

On the content side, I’d like the Substack to continue to be a labor of love. I’d like the podcast to continue to grow; I’ve said before my dream for the podcast would be to get inbounds from investors every time they take a new big position. I want activist investors to say “Ok, we just crossed 5% holdings in company X and it’s time to file our 13-D. Let’s line up an interview on CNBC for this morning and then really explain our thesis on Yet Another Value Podcast this afternoon.”

Andrew, thank you for the great interview! What is the best way for readers to follow or connect with you?

The best place to reach me is probably on Twitter (as a Twitter bull, I’m sure that’s what you love to hear!). Of course, people can follow Yet Another Value Blog or Yet Another Value Podcast, and responding to any of the emails / posts on there will go straight to my inbox.

Editor’s Note: Tegus Free Trial

Hi there, Edwin here. I reached out to the team at Tegus after a number of Idea Brunch interviewees recommended them and the Tegus team was kind enough to offer readers a free trial of their platform. Tegus is an insanely cool product that lets you find dozens of expert network call transcripts on any company in seconds. If interested, please email tom.preziose@tegus.co (.co not .com) and mention “Idea Brunch Tegus Free Trial” in the subject line.

If you enjoyed this Sunday’s Idea Brunch interview, please forward it to a few friends and encourage them to subscribe! And if you have feedback or want to suggest a great investor we should interview, please hit reply.

This newsletter is not investment advice and is for informational purposes only. You can reach the publisher by email at edwin@585research.com or on Twitter @StockJabber. This article is for premium subscribers of Sunday’s Idea Brunch newsletter. If this article was forwarded to you, please consider becoming a premium subscriber to receive interviews like this one every Sunday. Learn more here.

Good stuff, Andrew's great! 💚 🥃

Recently subscribed and so far underwhelmed!!